4.40 vs. 3.55: The Difference a Year Makes in Interest Rates

4.40 vs. 3.55: The Difference a Year Makes in Interest Rates

✉️ Want to forward this article? Click here.

One year ago, the average on a 30-year fixed-rate mortgage was 3.55 percent. On Thursday morning, Freddie Mac reported 4.40 percent with a 0.7 point as the average. So, how would the difference impact your mortgage payments?

Using this $839,000, three-bedroom rowhouse in Kent, we took a look at the difference in monthly payments, based on the today’s interest rates as compared to last year’s.

Let’s assume that in each case, the homeowner puts down 20 percent and takes out a loan for the remaining $671,200.

Here are the two interest rate scenarios.

August 2012: The average mortgage rate was 3.55 percent.

Monthly Mortgage Payment: $3,032

Total Outlay on Mortgage (Payment x 360 months): $1,091,520

August 2013: The average mortgage rate is 4.40 percent.

Monthly Mortgage Payment: $3,361

Total Outlay (Payment x 360 months): $1,209,960

So, the difference between a rate of 3.55 percent and 4.40 percent is about $329 a month or $118,440 over the life of the loan.

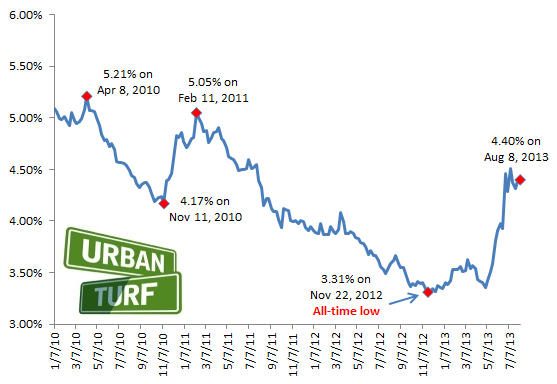

Here’s a look at the path of rates since January 2010:

See other articles related to: mortgage rates

This article originally published at https://dc.urbanturf.com/articles/blog/4.40_vs._3.55_the_difference_a_year_makes/7432.

UrbanTurf Listings showcases the DC metro area's best properties available for sale.

Most Popular... This Week • Last 30 Days • Ever

UrbanTurf is re-running its primer on property taxes which outlines a few things that... read »

The wait for Eataly in the DC area has been a long one.... read »

The Arlington County Board signed off on a pair of transformative residential project... read »

The plan to add a shade structure along the Cleveland Park commercial corridor has re... read »

DOGE doesn't seem dead yet; Monument buys Inn of Rosslyn; and Costco gas stations are... read »

DC Real Estate Guides

Short guides to navigating the DC-area real estate market

We've collected all our helpful guides for buying, selling and renting in and around Washington, DC in one place. Start browsing below!

First-Timer Primers

Intro guides for first-time home buyers

Unique Spaces

Awesome and unusual real estate from across the DC Metro

{kind=link}