What's Hot: Rising Costs Stall 434-Unit Takoma Metro Project | The DC-Area Luxury Market Is Playing By Its Own Rules

DC Renters Are Carrying the Region's Class A Apartment Market

DC Renters Are Carrying the Region's Class A Apartment Market

✉️ Want to forward this article? Click here.

Earlier this year, it was unclear how long the record-high absorption levels would last for new apartments in the metro area. A new Class A apartment report from Delta Associates indicates that demand in the District is carrying the market as absorption falls off elsewhere.

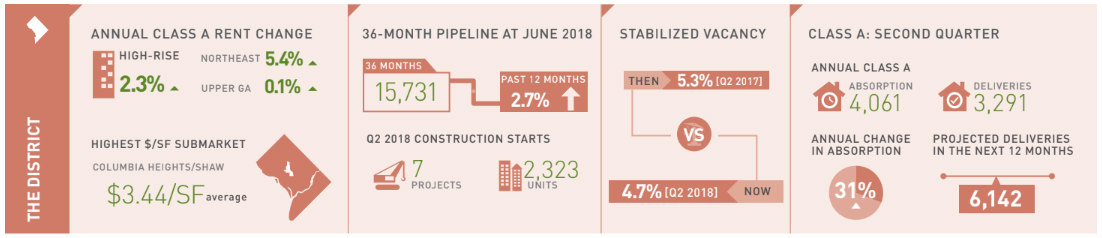

For the 12 months ending in June, 8,962 Class A apartments were absorbed — 45 percent of which were in DC proper. During the second quarter, 4,061 units were absorbed in the District, a 31 percent year-over-year increase; meanwhile, only 3,291 units delivered in the city. While new apartments continue to rent at a quick clip in DC, the news is not as rosy in other parts of the region.

In the last year, 3,988 Class A apartments delivered in Northern Virginia, yet only 2,566 apartments were absorbed, a 57 percent drop-off over the year. "The impact that the large influx of new supply has had on Northern Virginia has led to several months of elevated vacancy and slowed rent growth," the report states.

The skewed absorption levels in the region have resulted in an increased vacancy rate (4.1 percent) for Class A apartments, and while that will change, it could take awhile. "Given projected absorption and the delivery schedule of projects currently under construction, we expect the region-wide vacancy rate for stabilized Class A apartment properties will be 10 basis points lower in three years than it is today – resulting in a metrowide rate of 4 percent," the report states.

There are 37,340 apartments units currently in the 36-month pipeline regionwide. Ten projects, totalling 3,298 units, broke ground in the second quarter of this year; seven of those were in the District, accounting for 3,232 of the units.

Last quarter's projections that high supply would suppress rent growth persist, although high levels of absorption are expected to continue to balance these forces out and keep rents trending positively. In the District, rents are up by 2.3 percent year-over-year, led by a 5.4 increase in the Northeast submarket and a 5.3 percent increase in the Capitol Hill/Southwest/Riverfront submarket.

The latter super-neighborhood, along with the NoMa/H Street submarket, also accounts for over 70 percent of Class A rental inventory citywide, with over 11,300 units between them.

Here is a quick snapshot of average rents for high-rise Class A apartments in DC area sub-markets, as defined by Delta:

- Alexandria: $2,117 per month

- Central (Penn Quarter, Logan Circle, Dupont Circle, etc.): $2,866 per month

- Upper Northwest: $2,865 per month

- Columbia Heights/Shaw: $2,753 per month

- NoMa/H Street: $2,445 per month

- Capitol Hill/Capitol Riverfront: $2,517 per month

- Rosslyn-Ballston Corridor: $2,454 per month

- Silver Spring/Wheaton: $1,941 per month

- Bethesda: $2,769 per month

- Northeast: $2,067 per month

Note: The rents are an average of studios, one and two-bedroom rental rates at Class A high-rise buildings in the DC area.

Definitions:

Class A apartments are typically large buildings built after 1991, with full amenity packages. Class B buildings are generally older buildings that have been renovated and/or have more limited amenity packages.

See other articles related to: class a apartments, dc apartments, dc area market trends, delta associates, luxury apartments

This article originally published at https://dc.urbanturf.com/articles/blog/dc-renters-are-carrying-the-regions-class-a-apartment-market/14205.

UrbanTurf Listings showcases the DC metro area's best properties available for sale.

Most Popular... This Week • Last 30 Days • Ever

The wait for Eataly in the DC area has been a long one.... read »

EYA and the Washington Metropolitan Area Transit Authority have requested a two-year ... read »

While the broader DC-area housing market grapples with elevated mortgage rates and ca... read »

At the $1 million mark, DC's market offers strikingly different products depending on... read »

Justice Roberts selling Maryland home; bathroom danger; and what will future stadiums... read »

DC Real Estate Guides

Short guides to navigating the DC-area real estate market

We've collected all our helpful guides for buying, selling and renting in and around Washington, DC in one place. Start browsing below!

First-Timer Primers

Intro guides for first-time home buyers

Unique Spaces

Awesome and unusual real estate from across the DC Metro

{kind=link}