DC Bond Is Back

DC Bond Is Back

✉️ Want to forward this article? Click here.

DC’s Housing Finance Agency (DCHFA) has re-launched DC Bond, a program that makes affordable, fixed rate mortgages available to individuals and families seeking to purchase a home in the District.

In order to qualify, the borrower has to be buying their first home (which means that they can not have owned a home in DC in the last three years), the loan has to be for a primary residence and the maximum loan amount is $417,000. The borrower must have a minimum FICO score of 620 and conform to the following income limits: $57,500 for one person in the household; $65,700 for two people; $73,900 for three people, with more limits up to 8 people. There are areas of the city that are considered “targeted” and “non-targeted” for DC Bond, which causes variances in the formal guidelines and can lead to a number of exceptions to the aforementioned requirements.

DCmud provided additional details about the return of the program:

“The interest rate for borrowers is set at 5.25% with zero points and is currently only available as an FHA loan or a Veterans Administration loan, though financing without FHA or VA is being considered. The new bond requires all loans be purchased by Ginnie Mae. Funding for the program will likely run out come October, as it did last year, so any transaction would have to close prior to the fall.”

Qualifying homebuyers should welcome the return of DC Bond, which was available previously but ended last fall. There is very little reason not to take advantage of it, Rick Gibboney, senior loan officer with Bank of America told UrbanTurf. There is the possibility that mortgage rates could remain below the rate offered by DC Bond, in which case a homebuyer would be locked into paying above-market rates. But the consensus expectation is the opposite, that in fact rates will rise materially by the end of the year. Gibboney also noted that one of the big reasons to take advantage of the program is the $10,000 in down payment and closing cost assistance. However, he emphasized that this is not a credit, but a deferred, non-amortizing loan with a zero interest rate. When the owner sells the house, they have to pay the money back.

A few more things to keep in mind:

- There is a somewhat thinner pool of lenders with whom an interested homebuyer can work to get a DC Bond loan. Some lenders don’t like to do them because, as a quasi-governmental program, there is more paperwork and resources involved.

- The documentation on the website is thin and in fact has been known to be inaccurate. Anyone interested in actually pursuing this is encouraged to go with a loan officer that has experience dealing with the program.

See other articles related to: dc bond, first-time buyers, low-interest mortgage loans in targeted areas, mortgage rates

This article originally published at https://dc.urbanturf.com/articles/blog/dc_bond_is_back/1856.

UrbanTurf Listings showcases the DC metro area's best properties available for sale.

Most Popular... This Week • Last 30 Days • Ever

Janeese Lewis George appears to have won Tuesday's Democratic mayoral primary, puttin... read »

A new report shows that apartment rents in the DC region have fallen over the past ye... read »

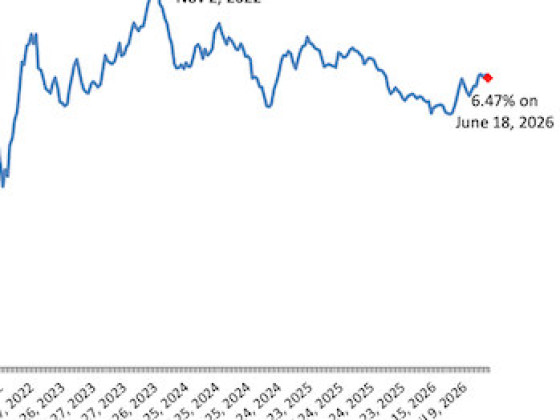

Freddie Mac reported Thursday that the 30-year fixed-rate mortgage averaged 6.47%, do... read »

Redbrick LMD has filed plans for a roughly 160-room hotel immediately adjacent to the... read »

On the heels of a new zoning regulation expanding alley housing around DC, a new resi... read »

DC Real Estate Guides

Short guides to navigating the DC-area real estate market

We've collected all our helpful guides for buying, selling and renting in and around Washington, DC in one place. Start browsing below!

First-Timer Primers

Intro guides for first-time home buyers

Unique Spaces

Awesome and unusual real estate from across the DC Metro

{kind=link}