First-Timer Primer: The Mortgage Pre-Approval Process

First-Timer Primer: The Mortgage Pre-Approval Process

As buyers get the itch to look for a home and start to venture out to open houses, it will behoove them to go through the pre-approval process. Pre-approval essentially consists of a lender going through various aspects of a homebuyer's background (credit history, income verification, etc.) to determine how much home they can actually afford (and how much of a loan they will be able to get).

Here is a quick Q&A that will help demystify the experience.

What information will a borrower need to submit for a pre-approval?

In general, a pre-approval applicant will need to submit last year's tax return, a current pay stub, and information about any other sources of income or assets (investments, retirement accounts, for example). In addition to assets, it is probably a good idea to give lenders a sense of all debts and monthly expenses. Lenders also like know where the down payment is coming from.

story continues below

loading...story continues above

How important is good credit?

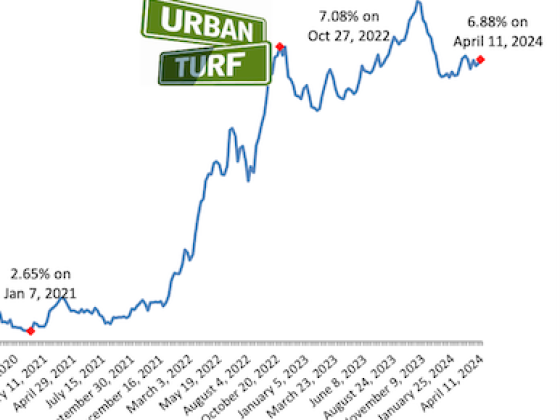

During the pre-approval process, the lender will also do a credit check. A "good" credit score is now considered 740 or higher. Drop into the high-600s and you may not get quite as low an interest rate as you may have wanted. Once you get below the mid-600s, it becomes more difficult to get a loan.

So, how much of a loan can I expect to get?

Generally, the rule-of-thumb that lenders use these days is to assume that the mortgage payment will be 33 percent of a borrower's gross monthly income, depending on other debts that the buyer carries. Typically, lenders don't want the total debt-to-income ratio to be more than 45 percent. (Interestingly, the old standard was 28 percent for housing, and 36 percent for total debts.)

For example, consider a $400,000 condo. Assuming a buyer will put down 20 percent ($80,000), and expects to pay $250 per month in taxes and $300 in condo fees, they will need an annual income of $73,000 to comfortably make their payments. However, they won't qualify for the same loan if they also have a $600 monthly car payment and $300 monthly student loan payment.

See other articles related to: first-timer primer, mortgages, pre-approval

This article originally published at https://dc.urbanturf.com/articles/blog/the-mortgage-pre-approval-process/15127.

UrbanTurf Listings showcases the DC metro area's best properties available for sale.

Most Popular... This Week • Last 30 Days • Ever

DC's homebuyer assistance programs can be a bit complex. This edition of First-Timer ... read »

When it comes to financing a home purchase, a 30-year mortgage is one of the most com... read »

Pocket listings are growing in popularity in the low-inventory market in the DC regio... read »

Plans for the development at a prominent DC intersection began nearly eight years ago... read »

The eight-bedroom, 35,000 square-foot home in McLean originally hit the market in 202... read »

DC Real Estate Guides

Short guides to navigating the DC-area real estate market

We've collected all our helpful guides for buying, selling and renting in and around Washington, DC in one place. Start browsing below!

First-Timer Primers

Intro guides for first-time home buyers

Unique Spaces

Awesome and unusual real estate from across the DC Metro

{kind=link}