First-Timer Primer: How Do Mortgage Payments Work?

First-Timer Primer: How Do Mortgage Payments Work?

This week, UrbanTurf is running a series of primers to help new homebuyers navigate all the ins and outs associated with purchasing their first home.

In this edition of First Timer Primer, we take a closer look at what you are actually paying for when it comes to sending in that monthly mortgage payment.

When purchasing a home these days, the most common mortgage that buyers take out is one that has a fixed interest rate over 30 years, though variable rate mortgages are becoming popular as interest rates rise to new heights.

story continues below

loading...story continues above

A mortgage will be paid down in equal monthly payments for the duration of the loan product period. The loan is generally composed of:

- Principal — This is the amount you borrowed, or the difference between the sales price and your down payment. Once your principal is paid off, you own the home outright.

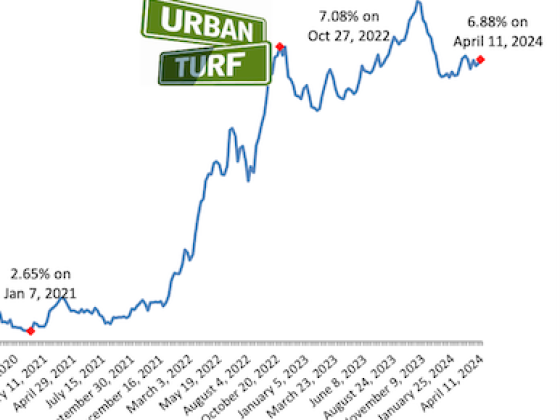

- Interest — In short, interest is a fee paid to the bank based on the size of the loan. Right now, the average on a 30-year fixed-rate mortgage is about 6.9 percent, and the total amount paid in interest over the life of a loan at this rate can be significant.

The interest is charged on the amount of loan principal that remains every month, so in the beginning, a higher proportion of your monthly payment will be interest. As time goes on, your payments will be, proportionally, more principal and less interest. This payment process is called amortization.

To provide a real life example of this, let’s look at a $600,000 loan with an interest rate of 6.6% and a total monthly payment of $3,832. In the first month, you’ll be paying interest on the full $600,000. This means $3,300 of your total payment will be interest, and you will pay down your principal by the difference: $532. The next month, you’ll be paying interest on the remaining principal or $600,000 – $532 = $599,468. The interest due will be slightly less than $3,300, and the principal paid will be more than $532. This trend continues for the duration of the loan, which is 360 months for a 30-year mortgage.

- Property taxes — On a $700,000 home in DC, total yearly taxes usually amount to about $6,000. This number varies depending on where you live. If your annual taxes were $6,000, you would pay $500 per month, and many banks wrap property tax payments into the monthly mortgage payment.

- Homeowner’s Insurance — This is a mandatory insurance policy that homeowners must take out on the full value of the property. Most mortgage lenders won’t issue a mortgage if the owner does not take out insurance. Typically, homeowner’s insurance is about 0.5 percent or more of the value of the home; for a home valued at $550,000, insurance could be about $220 per month. Like taxes, this payment will continue after your mortgage is paid off.

As a final note, you can always make mortgage payments that are larger than the set amount and pay off your mortgage sooner than the life of the loan, thus paying a smaller amount in total interest.

Similar Posts:

- First Timer Primer: How Much Cash Do You Need to Buy a House?

- First-Timer Primer: The Mortgage Pre-Approval Process

See other articles related to: first-time buyers, first-timer primer, mortgages

This article originally published at https://dc.urbanturf.com/articles/blog/first_timer_primer_how_do_mortgage_payments_work/6649.

UrbanTurf Listings showcases the DC metro area's best properties available for sale.

Most Popular... This Week • Last 30 Days • Ever

DC's homebuyer assistance programs can be a bit complex. This edition of First-Timer ... read »

When it comes to financing a home purchase, a 30-year mortgage is one of the most com... read »

Pocket listings are growing in popularity in the low-inventory market in the DC regio... read »

Plans for the development at a prominent DC intersection began nearly eight years ago... read »

The eight-bedroom, 35,000 square-foot home in McLean originally hit the market in 202... read »

DC Real Estate Guides

Short guides to navigating the DC-area real estate market

We've collected all our helpful guides for buying, selling and renting in and around Washington, DC in one place. Start browsing below!

First-Timer Primers

Intro guides for first-time home buyers

Unique Spaces

Awesome and unusual real estate from across the DC Metro

{kind=link}