Low Price, Long Process: The Truth About Short Sales

Low Price, Long Process: The Truth About Short Sales

Homeowners who owe more money on their mortgage than the current value of their home have few options, particularly if they must sell the home because they can no longer afford to make the payments. In order to avoid foreclosure, some owners have been able to negotiate a short sale, which means that the lender agrees to accept less than the full amount of the mortgage principal as payment.

The allure of a short sale to buyers is that they can sometimes pay below market price for a home. However, the downside is that this buying process can be quite long and unpredictable. Unlike a standard real estate transaction between a buyer and a seller (and their representatives), a short sale is a three-way negotiation in which the buyer’s offer must be accepted by both the seller and the seller’s lender. Below we point out some important things to keep in mind if you are considering a short sale.

Time

The short sale buying process can last anywhere between 60 days and a year. Because of the uncertainty of this process, renters should make sure that they can go to a month-to-month lease so they are not tied to a specific settlement date. If you have a goal of moving within a couple of months or are committed to a certain date, then a short sale is not for you.

Financing

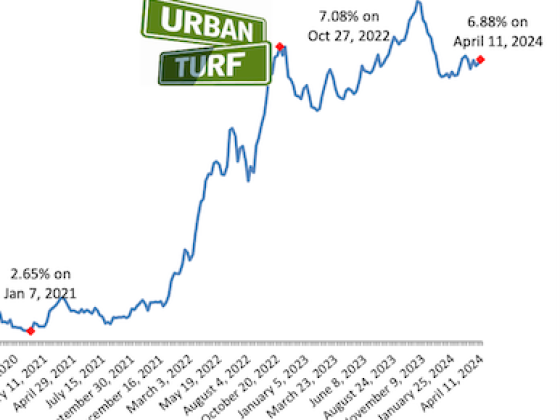

Buyers in traditional transactions start by getting a preapproval for a mortgage (unless they can pay cash), and short sale buyers should do the same. Unfortunately, short sale buyers usually are at a disadvantage when it comes to locking in a specific loan rate. While buyers in a normal transaction can lock in a loan rate for 30 days or a little longer, the uncertainty of a short sale makes a lock-in nearly impossible. Preapproval for a loan can also be limited to a certain time period, so buyers need to know how long their loan approval will last and reapply if they are still waiting for word on the short sale when the first approval expires.

Condition

Short sales are usually in better shape than foreclosures, but buyers still need to expect that the home will be sold “as is”. Be sure to pay for a home inspection that will give you a full rundown on the condition of the home.

Making an Offer

When deciding how much to offer, buyers should consider not only what the sellers will accept but also what the bank will accept. An offer close to what comparable homes are going for in the area, discounted to allow for repairs, is more likely to be accepted than a low-ball offer. However, if there are no other prospective buyers, a lower offer may be acceptable to all sides.

Buyers can also put a time frame in their offer which allows them the option to withdraw it if approval has not been given fast enough.

Professional Help

Work with a CDPE (certified distressed property expert) who has extra training in short sales and foreclosures and may be able to push the short sale closer to settlement. In addition, retain the services of a reliable settlement attorney who can expedite the short sale and the release of any liens against the property.

See other articles related to: distressed real estate, home buying, short sales

This article originally published at https://dc.urbanturf.com/articles/blog/low_price_long_process_the_truth_about_short_sales/1518.

Play to hear Jen in her own words

UrbanTurf Listings showcases the DC metro area's best properties available for sale.

Most Popular... This Week • Last 30 Days • Ever

DC's homebuyer assistance programs can be a bit complex. This edition of First-Timer ... read »

When it comes to financing a home purchase, a 30-year mortgage is one of the most com... read »

Pocket listings are growing in popularity in the low-inventory market in the DC regio... read »

Margarite is a luxury 260-apartment property known for offering rich, high-end reside... read »

The owner of 700 Monroe Street NE filed a map amendment application with DC's Zoning ... read »

DC Real Estate Guides

Short guides to navigating the DC-area real estate market

We've collected all our helpful guides for buying, selling and renting in and around Washington, DC in one place. Start browsing below!

First-Timer Primers

Intro guides for first-time home buyers

Unique Spaces

Awesome and unusual real estate from across the DC Metro

{kind=link}