From Our Archives: Credit Score: Do You Know Yours?

From Our Archives: Credit Score: Do You Know Yours?

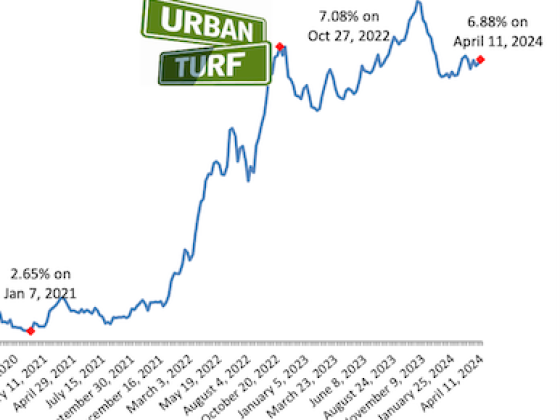

With the possibility that we might see sub-4 percent loan rates on this coast some point soon, it seemed fitting to dig into our archive and re-publish our article on improving your credit score, as a good score is critical to being approved for an attractive loan these days.

(Originally published on June 12, 2008)

Credit history is generally avoided as a topic of conversation at all costs. This is because the large majority of us are in debt, some worse off than others. There are those of us who miss the occasional credit card payment and let the phone bill go two months before paying. No big deal. Then there are those of us who have a mountain of credit card debt that has amassed since college and rarely pay the telephone or cable bill before the credit bureaus come looking.

Depending on which of these camps you are in, your credit score can be affected for the better or worse. And when you are setting out to buy an apartment or a house, chances are you will need to apply for a loan. Before you can be approved for a loan, you need to have your credit score calculated.

A credit score is essentially a number between 300 and 850 that indicates whether a person has good or bad credit based on their credit history. The higher the number is, the better the credit history and vice versa. Americans are entitled to one free credit report every 12 months from one of three credit bureaus: Experian, TransUnion or Equifax.

Not paying bills on time is the most common thing that can adversely affect your credit score. High balances on credit cards and overdue loan payments are also factors.

“If you have three cards, each allowing a $5,000 credit limit, having $1,500 on all three rather than having $4,500 on just one will certainly help improve your score, ” Norman Calvo of Universal Mortgage told UrbanTurf.

Having too many credit inquiries also can hurt your score. In other words, if you are one of those people that waits several months to pay your bills, and the notices come that your service might be cut off, your credit score will take this into account.

A credit score is a crucial standard used by mortgage lenders as an indicator of how likely you are to pay off your debts. For an excellent score in the range of 760-850, interest rates can be as low as 5.9 percent for your loan (Note: As of 3/09, this rate has dropped to 4.9 percent), according to myfico.com. However, if your score is in the 600 range, then you are looking at a rate closer to 12 percent.

If you find yourself saddled with debt, do not despair. Here are some tips from Universal Mortgage that will help lower your score.

- Only worry about paying off past due balances and other debts that have occurred in the past two years because items more than two years old have little effect on your credit score. Even if your credit was poor prior to the last two years, present good credit shows that you have made adjustments to your spending and payment habits, sort of like a reformed addict.

- Do not close credit card accounts that you don’t really use. It shows restraint that you haven’t been going on spending sprees and that you are aware of your credit obligations. “Its kind of like someone who knows to ‘save’ for a rainy day,” Calvo told UrbanTurf.

- Instead of trying to pay off the debt on all your credit cards, try and move some of the debt around so that it is evenly distributed on various cards. The ratio of debt to credit limits should be about 30 percent of the available credit or less.

This article originally published at https://dc.urbanturf.com/articles/blog/from_our_archives_credit_score_do_you_know_yours/679.

UrbanTurf Listings showcases the DC metro area's best properties available for sale.

Most Popular... This Week • Last 30 Days • Ever

DC's homebuyer assistance programs can be a bit complex. This edition of First-Timer ... read »

When it comes to financing a home purchase, a 30-year mortgage is one of the most com... read »

Pocket listings are growing in popularity in the low-inventory market in the DC regio... read »

Plans for the development at a prominent DC intersection began nearly eight years ago... read »

The eight-bedroom, 35,000 square-foot home in McLean originally hit the market in 202... read »

DC Real Estate Guides

Short guides to navigating the DC-area real estate market

We've collected all our helpful guides for buying, selling and renting in and around Washington, DC in one place. Start browsing below!

First-Timer Primers

Intro guides for first-time home buyers

Unique Spaces

Awesome and unusual real estate from across the DC Metro

{kind=link}