Ask an Agent: Questions That Arise When Shopping for a Mortgage

Ask an Agent: Questions That Arise When Shopping for a Mortgage

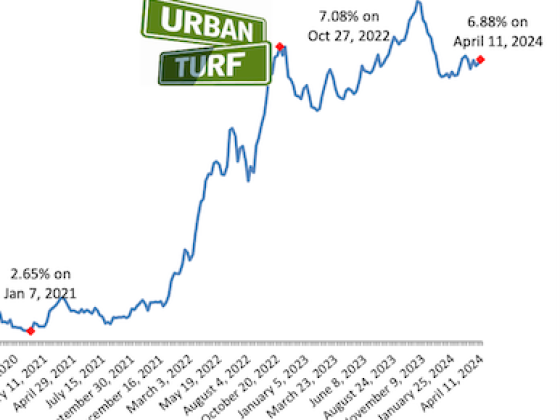

In this installment of Ask An Agent, we switch gears a little bit as this week’s question(s) is more focused on mortgages. A reader wonders if a home buyer needs to submit applications to all potential lenders and if it even makes sense to submit these applications given that you can find detailed rate information on lenders’ websites. Prosperity Mortgage’s Tom O’Keefe offers up some insight.

Question: I have two questions about shopping around for mortgages. First, is a prospective homeowner supposed to submit pre-approval applications or mortgage applications to each potential lender when shopping? (Mortgage applications are expensive — $300 — so it seems odd to me that people will submit more than one application.) Second, why bother submitting numerous applications when you can get detailed rate information from potential lenders’ websites (or from one of their representatives)?

Answer: Most lenders do not require an upfront fee to pre-approve a homebuyer. The first question to ask when interviewing a potential lender is “What is the cost of a pre-approval?” If the answer is more than $0, move on to another lender. Once the homebuyer is pre-approved, identifies a property, and a purchase contract is ratified, most lenders require an application fee to proceed with the formal approval and appraisal order. This is the point where homebuyers choose the lender who they plan on using for their purchase.

Typically, multiple pre-approval letters are not required, so applying to more than one lender ahead of having a ratified contract does not make much sense. In most, if not all cases, a buyer cannot lock in an interest rate until they produce a fully ratified contract to their lender. Therefore, if a buyer wants to shop rates and fees, they should do it once they have a contract in hand. Using bank or lender websites is a good way to track rate trends, but it is not recommended for rate quotes. An accurate rate quote is very specific to each and every buyer. It takes into account credit score, down payment, property type, number of days required to close, and the type of mortgage (i.e. conventional vs. FHA). Therefore, rate quotes should be given in person, via email, or over the phone by a mortgage professional who can take into account all of these factors.

See other articles related to: ask an agent

This article originally published at https://dc.urbanturf.com/articles/blog/ask_an_agent_questions_that_arise_when_shopping_for_a_mortgage/1361.

UrbanTurf Listings showcases the DC metro area's best properties available for sale.

Most Popular... This Week • Last 30 Days • Ever

DC's homebuyer assistance programs can be a bit complex. This edition of First-Timer ... read »

When it comes to financing a home purchase, a 30-year mortgage is one of the most com... read »

Pocket listings are growing in popularity in the low-inventory market in the DC regio... read »

Plans for the development at a prominent DC intersection began nearly eight years ago... read »

The eight-bedroom, 35,000 square-foot home in McLean originally hit the market in 202... read »

DC Real Estate Guides

Short guides to navigating the DC-area real estate market

We've collected all our helpful guides for buying, selling and renting in and around Washington, DC in one place. Start browsing below!

First-Timer Primers

Intro guides for first-time home buyers

Unique Spaces

Awesome and unusual real estate from across the DC Metro

{kind=link}